Progressive Powers Ahead: Strong Growth and Profits in Q1

Strong pricing discipline and market share gains highlight another stellar quarter

The Progressive Corporation (PGR) has recently published its preliminary Q1 results. As has been the case for quite a few quarters, they defy imagination.

It is the combination of excellent underwriting results and explosive growth at scale that keeps me wondering.

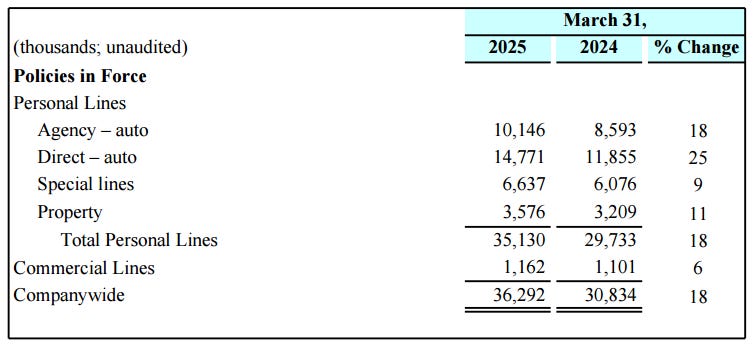

The next slide shows a more granular picture of what is going on.

Before analyzing, here are some quick takeaways:

We can expect a strong quarter from Berkshire Hathaway’s Geico as well, which is a major component of BRK’s operating earnings.

Property lines did well in Q1. For 2024, the property expense ratio was 29.0%, and we should see gradual improvement here as the business scales up. In Q1, the expense ratio was 28.8%. The progress may seem tiny, but it is just the beginning.

Property’s NPE growth rate was 9% in Q1 vs. 17% in full 2024. The company may be more selective now in picking property risks and is more focused on profitability vs. growth for these lines. As a reminder: in 2024, for the first time, Property was profitable for the full year.

In Autos, Progressive underwriting was again better for Agency vs Direct. The Agency’s lower expense ratio (18.3% vs 21.3%) probably means that brokers remain cheaper than advertising.

Progressive’s float

The words “insurance float” are typically associated with Berkshire first and with Fairfax second. Both companies report float and emphasize its profitability. Progressive does not mention “float” in its reporting (at least I did not notice it) and does not position itself as an investor. Nevertheless, it is quite instructive to present some stats about Progressive’s float. They will blow you away.