Legal & General's Deep Dive: On the Path to Becoming an Alt Manager

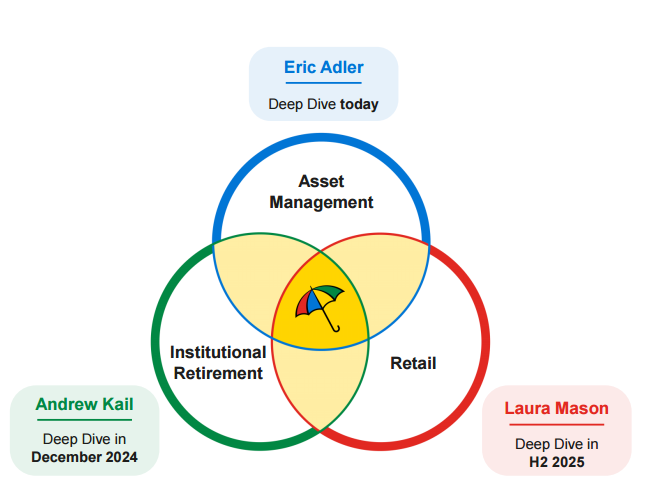

Legal & General’s (LGEN in London, LGGNY, and LGGNF in the US) second deep dive was devoted to Asset Management (“AM”), one of its three segments. After this presentation, there is no doubt left that LGEN is on its way to becoming an asset-heavy alt manager similar to Apollo (APO) but with certain distinctive traits. This strategy is expected to have major consequences for LGEN’s stock, which we will analyze at the end of this article. US investors should keep in mind that there is no withholding tax in the UK and LGEN’s dividends are qualified for reduced tax rates.

LGEN is a venerable life insurer consisting of three segments.

Institutional Retirement executes PRTs (pension risk transfer, aka group annuity) mostly in the UK and is the biggest segment. Retail sells annuities and other life insurance products to individuals in the UK. We will talk mostly about AM, which manages funds of both insurance segments as well as of third parties. I posted about LGEN several times, with “A 9% Yielding Stock Poised for 20% Annual Returns” being the latest. Please check my posts to better understand the company.

To get the most out of this article, it helps to have a basic understanding of the industry and its key players.

If you are unfamiliar with alternative asset managers, check my free “Primer on Alternative Asset Managers”.

To understand Apollo’s revolutionary model for life insurance that LGEN follows now, check my free “Magician Apollo Transforms Life Insurance”

Background

For the last decade or so, LGEN’s stock has remained stagnant despite increasing dividends every year. When I invested and started writing about the company at the end of 2023, the yield was more than 8% with 5% annual dividend growth. Investors were mostly yield-seekers.

In January 2024, Anthony Simoes was appointed CEO, and within a few months, he began reshaping the company. His key initial decisions included:

Selling non-core assets that were either not related to the insurance business or did not have sufficient scale.

Historically, LGEN had two asset management segments in charge of traditional and alternative investments, respectively. They were merged into one AM. It took almost a year to hire Eric Adler to lead the segment. He was in charge of Prudential’s private alternatives before his appointment.

Dividend growth was reduced from 5% to 2%, but the difference—and more—was redirected toward share buybacks, which were absent before.

The then-existing shareholder base did not like limiting dividend growth, and the stock went on sale - I bought most of my shares at ~9.5% yield. My investment thesis was rather simple. I sensed that LGEN was laying the ground to transform itself to follow Apollo’s model and already had both a life insurer and an asset manager under one roof. If LGEN succeeded in its transformation, investors would continue receiving strong dividends and would also likely enjoy stock appreciation. Under this scenario, buybacks made sense. Otherwise, investors would just collect high dividends.

The transformation of AM is the cornerstone of Mr. Simoes’s long-term strategy. While Institutional Retirement remains LGEN’s current cash cow, it faces an existential risk: the supply of defined benefit (“DB”) corporate plans eligible for PRT is finite, both in the UK and globally. Most employers have already transitioned to defined contribution (“DC”) plans, closing the pipeline of new DB liabilities.

At the current pace, the PRT market has perhaps another decade before it begins to taper off. After that, legacy pension liabilities will continue to generate spread-related earnings for decades until fully exhausted. For LGEN, long-term growth cannot rely on PRT alone. Retail seems too small to replace PRT as the company’s growth engine. AM, on the contrary, is already big and represents LGEN’s best chance to reinvent itself.

Presentation

It consists of 62 slides presented by Anthony Simoes, Eric Adler, and CFO Jeff Davies, plus the Q&A session. I will emphasize the presentation’s main points instead of following it sequentially.

LGEN is the biggest asset manager in the UK and one of the biggest in the world.